A cornerstone of the global theatrical industry just changed hands for $70 million, and almost nobody blinked. That may turn out to be a mistake.

By Julien Marcel | CEO, Cine Group & Publisher, Boxoffice Pro France

On May 27, Advaya Capital completed the purchase of Comscore Movies and announced that the business would revert to its pre-merger name, Rentrak. The base price, disclosed in a Securities and Exchange Commission filing, is $70 million in cash. Two industry veterans join the board: Chris Aronson, the former domestic distribution chief at Paramount and 20th Century Fox who founded Rentrak Theatrical, and Arturo Guillén, the former global managing director of Comscore Movies. Advaya is led by managing partner Anant Gupta, a former Nielsen board member. That, in essence, is the news.

What is striking is how little of it registered. The deal was widely and accurately reported, but the conversation has so far stopped at the facts of the announcement. There has been little debate, few analysts weighing in, and almost no exploration of what the change of ownership means for an asset that sits at the very center of the theatrical business. Everyone duly noted the reassuring presence of Aronson and Guillén, and the return to the Rentrak name. Back to the Future, or Groundhog Day?

Two questions sit underneath that indifference. First, has everything changed (the ownership) precisely so that nothing changes? Second, why so little curiosity about the fate of one of the cornerstones of the theatrical industry?

A Giant Priced Like a Footnote

Start with the contrast that should have raised more eyebrows. Comscore Movies occupies a dominant position as the industry’s currency: transaction-level data from roughly 34,000 theaters and more than 200,000 screens across 70-plus countries, covering about 95% of the global box office and close to 100% of the North American market. Studios, distributors, and exhibitors rely on it for release strategy, financial settlements, talent compensation, and licensing. It is, almost literally, the scoreboard of the industry.

And yet the whole thing sold for $70 million. That is roughly 1.8 times the segment’s 2025 revenue and about 5.5 times its operating income. Having cornered the market on the industry’s measurement currency, those are the multiples of a tired, no-growth business, not of critical infrastructure.

The Lifeboat Nobody Noticed

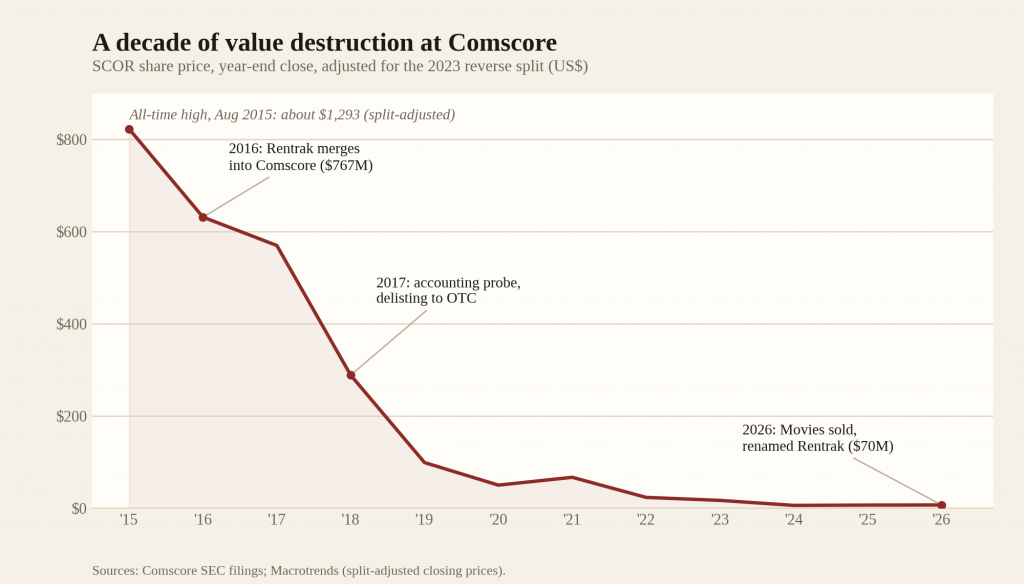

To understand the price, you have to look at the seller. Comscore has lived through a genuine industrial catastrophe since the 2016 merger that brought Rentrak into the group, a deal worth $767 million at the time. What followed was an accounting investigation, a restatement, a move to the over-the-counter market, an SEC settlement, years of restructuring, a preferred-equity recapitalization, and, eventually, a one-for-twenty reverse stock split. The chart below tells the rest.

Comscore (SCOR) share price, year-end close, adjusted for the 2023 reverse split. Sources: Comscore SEC filings; Macrotrends. The combined company, worth several billion dollars at the 2016 merger, now has a market capitalization of roughly $100 million, barely more than the price its profitable core just fetched on its own.

Crucially, the Movies business was never core to where Comscore wanted to go. The group’s strategic story was about cross-platform and connected-TV currency, a fight against Nielsen for the living room. Theatrical measurement was the quiet, profitable corner that funded the ambition, and it stayed below the radar accordingly. The result was a company that gradually lost the market’s attention: fewer analysts, fewer comments, and almost none on the Movies segment specifically.

Which is why the SEC numbers landed like a small revelation. In 2025, the Movies business generated about $38 million in revenue (roughly 11% of the group) and more than $12 million in operating income, with a 33% operating margin. Strip it out, and the rest of Comscore ran an operating loss. In other words, the segment everyone ignored accounted for more than the group’s entire operating profit.

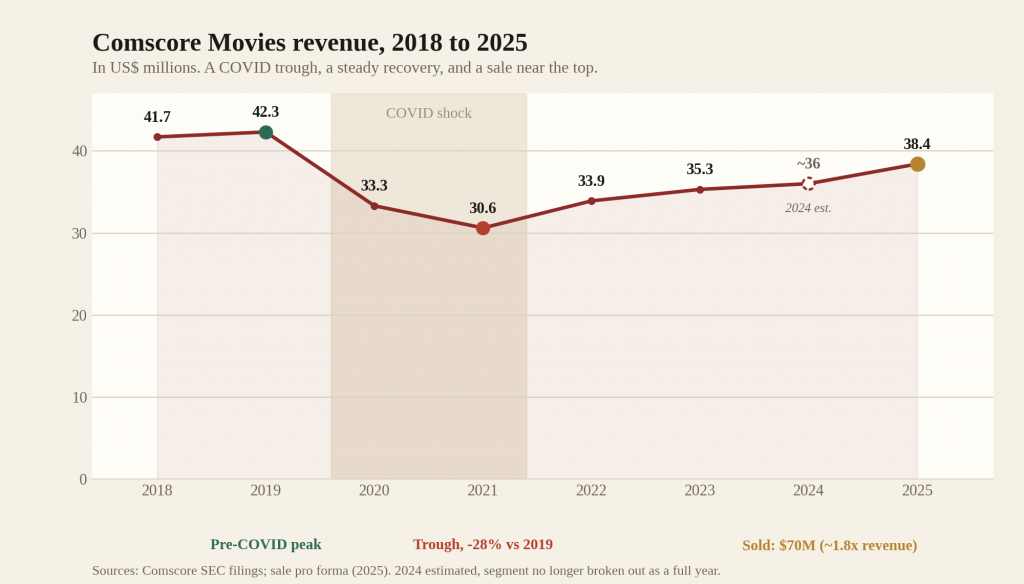

Comscore Movies revenue, 2018 to 2025 (US$ millions). Sources: Comscore SEC filings and the sale pro forma. The segment fell about 28% in the pandemic, recovered steadily, and was sold near the top of that recovery at roughly 1.8 times revenue. 2024 is estimated, as the segment was no longer broken out as a full year.

The True Weight of the Deal

For Comscore, the logic is deleveraging that could no longer be postponed. The proceeds were used to repay its Blue Torch term loan in full, around $40 million, clearing the most pressing pressure on the balance sheet. The company even booked a small accounting loss on the sale, because the carrying value of the assets exceeded the price. That is the signature of a forced seller, and it explains why the number otherwise looks far too low.

For what interests us more, the future of Rentrak, the deal could mark the start of a genuinely ambitious chapter, for four reasons.

The People

Aronson and Guillén are not decorative. They carry the confidence of both the operating teams and the wider industry, which matters enormously for an asset whose only potential obstacle is trust.

The Timing

This arrives at the dawn of the AI era, where data is king. Rentrak has always sat on far more data than it was ever able to exploit. AI is precisely the tool that could change that, turning a passive scoreboard into predictive and prescriptive intelligence, and creating value that simply was not capturable before.

The Potential

“The business has been seriously under-managed for years. For some time it had no clearly designated leader, a gap that may be filled as early as CineEurope. That is bad history, but it also provides unusually fertile ground: the easiest businesses to improve are the ones that have been starved of attention. That opening provides unusually fertile ground: the easiest businesses to improve are those that have not yet reached their full potential.

The New Owner

Moving into the hands of a fund led by a measurement expert, a former Nielsen director, you can reasonably expect a sharp inflection and a renewed sense of ambition rather than passive stewardship.

A Bigger Story Than Meets the Eye

A currency draws its value from neutrality and universal acceptance rather than from analytical firepower, so the AI upside has to be built, not assumed. And a sponsor that buys an established leader at such a favorable price always has the option to harvest it rather than reinvest. Those are real risks, and the industry would be wrong to ignore them.

But weigh the whole picture. You have a uniquely defensible asset, finally separated from a group that treated it as an afterthought, handed to people the industry trusts, backed by an owner who understands measurement from the inside, at the precise moment when AI is turning dormant data into the most valuable raw material in media. Rentrak has always held far more information than it ever managed to monetize. For the first time in a decade, it has both the freedom and the reason to use it.

So Lampedusa’s line from The Leopard, everything must change so that everything can stay the same, is the trap to avoid here, not the prophecy to expect. The name change is the cosmetic part. The substance: ownership, focus, ambition, and timing, is where the real shift sits. This is not Groundhog Day. It is closer to Back to the Future: a return to the Rentrak name that is really a run at what the business could have been all along.

Read that way, the $70 million line item that the market greeted with a shrug may prove one of the more consequential moves in the theatrical value chain this decade. No news? Quite the opposite. The sleeping beauty just woke up.

Julien Marcel is the CEO of Cine Group, the French leader in ticketing and digital marketing for cinemas, and the publisher of Boxoffice Pro France.

Share this post